The Data Disagrees With the ‘Google Is Dying’ Narrative

Every earnings call, every LinkedIn thread, every tech-media headline tells the same story: AI is eating Google’s lunch.

The actual numbers say something different.

Berkshire Hathaway’s Q1 2026 13F filing showed the firm tripled its Alphabet stake to roughly $16.6 billion, making Google the firm’s fifth-largest holding (IBTimes, 2026). It was the first quarterly disclosure under new CEO Greg Abel. The institutional money is moving the opposite direction from the narrative.

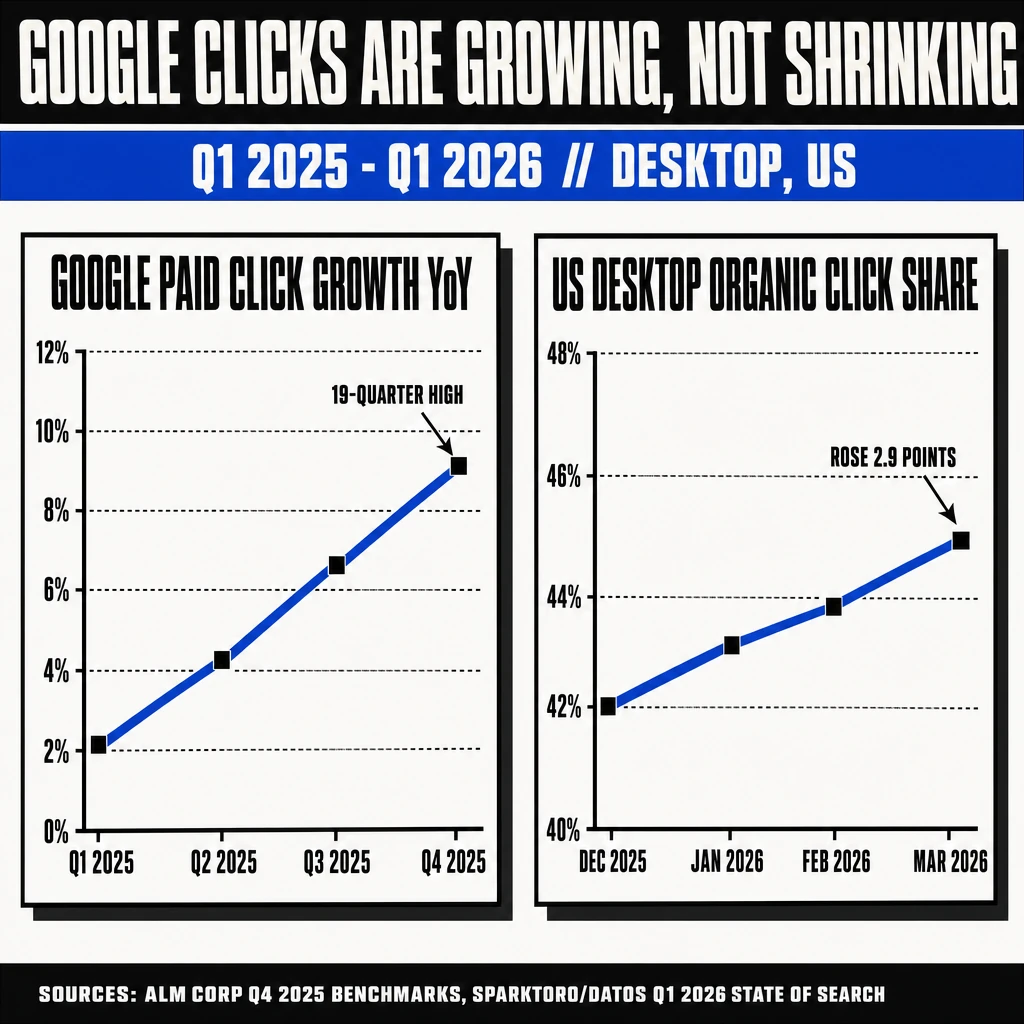

The user-behavior data agrees. US desktop organic click share rose from 42.0% in December to 44.9% in March (SparkToro/Datos, 2026). Google search ad clicks grew 9% year-over-year in Q4 2025, a 19-quarter high (ALM Corp, 2026). Alphabet broke $400 billion in annual revenue for the first time.

The disconnect between what the media is selling and what the data says is now wide enough to be its own story.

Key Takeaways

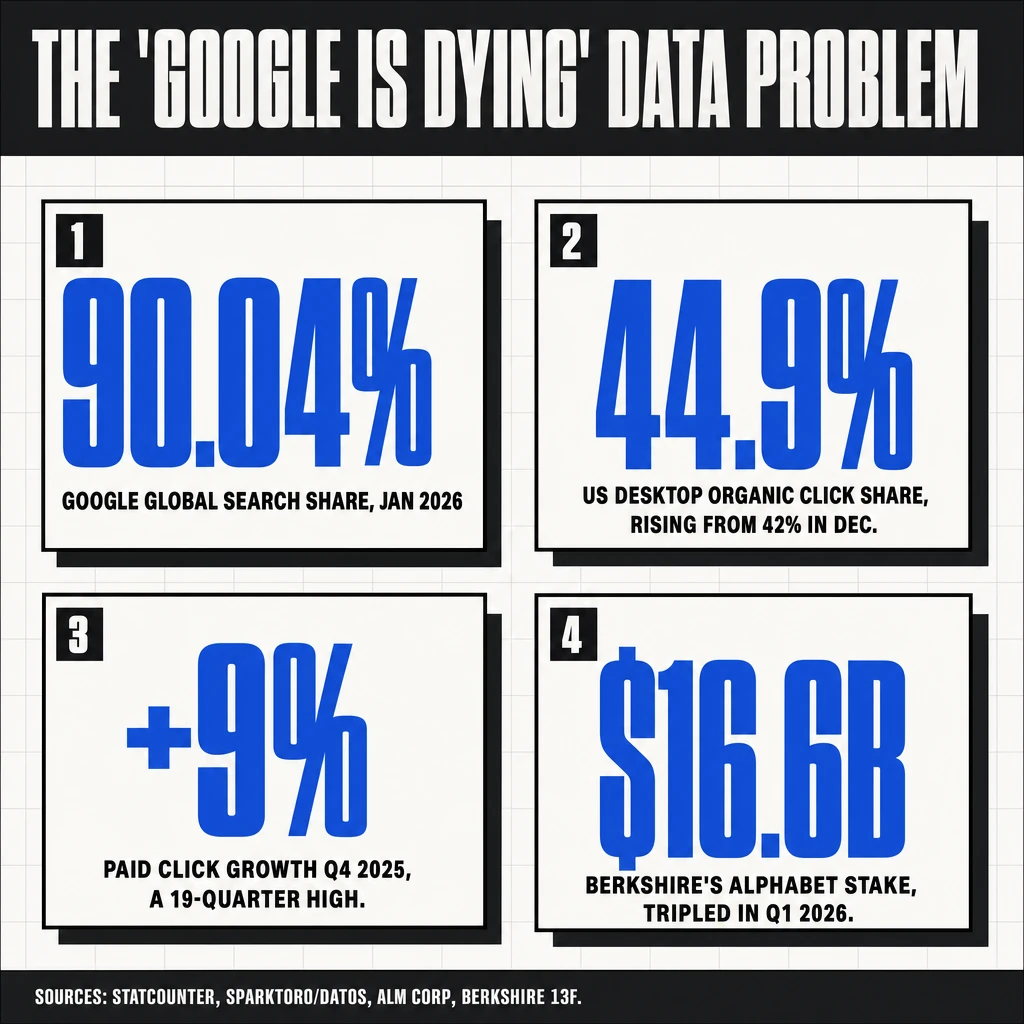

- Berkshire Hathaway tripled its Alphabet stake in Q1 2026 (204% increase in shares held). Google is now the firm’s fifth-largest holding at ~$16.6 billion (IBTimes, 2026).

- Google’s global search market share was 90.04% in January 2026 and 90.02% in April 2026 (StatCounter). The desktop figure is 79.1%, the lowest in 20+ years, but mobile share is 94.6%.

- US desktop organic click share rose 42.0% → 44.9% from December 2025 to March 2026 (SparkToro/Datos). EU/UK held in a 44-48% range over the same period.

- Google paid clicks grew 9% YoY in Q4 2025, a 19-quarter high. Search ad revenue grew 17%. Alphabet broke $400 billion annual revenue (Alphabet 10-K, 2026).

- AI Overviews reached 1.5 billion monthly users, and Pichai stated on the Q4 2025 earnings call that AI Overviews are “driving greater usage” of Search overall.

- The “Google is dying” narrative is selling badly against the data. The contrarian read is the boring one: Google is doing fine.

The Numbers That Should End the Debate

I keep four numbers on a card near my desk because the conversation about Google in 2026 usually skips them.

Number one: 90.04%. Google’s global search market share across all devices in January 2026 (StatCounter, 2026). Down a fraction of a point from the year before, still higher than any single competitor by 80+ percentage points. Bing held roughly 4%. Everyone else combined held the rest.

Number two: 44.9%. US desktop organic click share in March 2026, up from 42.0% in December (SparkToro/Datos). The “users are abandoning organic clicks” story does not survive contact with the desktop data.

Number three: 9%. Year-over-year growth in Google search ad clicks in Q4 2025 (ALM Corp, 2026). This was a 19-quarter high. If users were leaving Google for AI tools, this is not the number you would see.

Number four: $16.6 billion. The dollar value of Berkshire Hathaway’s Alphabet position after the firm tripled its stake in Q1 2026 (IBTimes, 2026). Berkshire does not chase trends. The position size is a statement about what the firm’s analysts believe about Google’s structural position over the next decade.

The Berkshire Signal

Berkshire Hathaway’s 13F filing on May 15, 2026 disclosed the firm raised its Alphabet position by 204% during the first quarter (BBAE, 2026). The new position is 54.2 million Class A shares plus 3.6 million Class C shares, valued at ~$16.6 billion.

The detail that matters: this was the first quarterly disclosure under Greg Abel, who took over from Warren Buffett on January 1, 2026.

New management at Berkshire. New largest moves. The biggest single position change was tripling Alphabet. The signal is loud whether or not the analyst calls are.

Berkshire’s thesis on a stock is rarely about quarterly news. It is about structural advantages that hold for ten years or more. The 13F effectively says the firm believes Google’s structural moats (distribution through Chrome and Android, advertising marketplace, search index quality, infrastructure) will survive the AI assistant era intact.

The institutional money has access to the same earnings calls everyone else does. The fact that they tripled their position after reading those calls is itself a data point.

Why Desktop Organic Clicks Are Going Up, Not Down

The “Google is dying” story usually leans on the organic click decline narrative.

That narrative is mostly a mobile story. Mobile zero-click rate sits at 77%; desktop is 56% (SparkToro/Datos, 2026). The 21-percentage-point gap is the single biggest piece of context most coverage skips.

And on desktop specifically, the recent trend reversed. US desktop organic click share rose from 42.0% in December 2025 to 44.9% in March 2026 (SparkToro/Datos). EU/UK held in a 44-48% range over the same period.

My read on what changed: Google made the SERP more clickable, not less.

The visible product moves support this. FAQ rich results died in May 2026. AI Overview density was trimmed in certain verticals where click impact was severe. Shopping units expanded. Each individual change was small. The aggregate effect is a SERP that surfaces more clickable destinations per query than it did a year ago.

I covered the practitioner-side implications in my post on Google’s AI content rules. The short version: Google’s documentation describes the world they want, and the SERP changes describe the world they need.

The Paid-Click Boom Tells the Same Story

Google text ad clicks grew 9% YoY in Q4 2025. That was the highest quarterly growth in nineteen quarters. Spend rose 11%, implying only ~2% CPC inflation; the click volume drove almost all the revenue growth.

Search ad revenue grew 17% in the same quarter. Alphabet broke $400 billion in annual revenue for the first time.

If users were truly migrating to AI assistants, the paid-click number would be flat or declining. Advertisers do not bid up clicks to a destination users are leaving.

The simplest explanation is the one matching the data: search session counts are growing, the average user is performing more queries per session, and a slightly larger share of those queries result in a paid click than a year ago.

The Skeptical Read (Where the Narrative Is Partially Right)

The “Google is dying” narrative is not entirely wrong. It is mostly wrong, but a few of its component claims hold up.

Desktop search share is at a 20-year low at 79.1% (StatCounter, 2026). That is a real decline. Bing has expanded desktop presence by over 151% over the last decade. AI search platforms grew 225% year over year.

The growth percentages on AI tools look terrifying until you check the base. The Datos Q1 2026 report flagged AI tool usage at under 2% of all visit events (PPC Land, 2026). Growing 225% from 0.8% gets you to 2.6%. Not yet a substitution event.

AI Overviews are a real measurement problem for specific verticals. Headphone-category organic click share dropped from 73% to 50% between January 2025 and January 2026 (ALM Corp, 2026). If a publisher is in a vertical where AI Overviews are dense, the local experience does not feel like “Google is fine.”

The honest framing: Google is doing fine in aggregate, hurting in specific verticals, and not yet meaningfully threatened by AI assistants in terms of share. Both things can be true.

What This Means for SEO Practitioners

Operational implications worth acting on this quarter:

- Do not pivot the program around a “Google is dying” thesis. The data does not support it at the level most SEO budgets are decided.

- Check your vertical-specific impact, not the aggregate. If you are in a heavy-AI-Overview vertical, the local experience is different from the aggregate. Audit by query category before assuming the macro story applies to you.

- Treat AI tool optimization as a long-term entity-building project, not a near-term traffic source. Under-2% of all visit events going to AI tools means even rapid growth keeps the channel small for another 12-24 months.

- Watch what the SERP is doing, not what the docs are saying. The SERP changes (FAQ rich result death, AI Overview trims, shopping unit expansion) are leading indicators. Google’s documentation is a lagging indicator for what is actually shipping.

- Read what institutional money is doing. The Berkshire 13F is publicly disclosed quarterly. Quiet capital allocators give clearer signals than loud product analysts.

None of this means ignore AI search. It means right-size the response to the actual shape of the data, not the shape of the headlines.

FAQ

Sources & References

- IBTimes. “Berkshire Hathaway’s Top 20 Holdings Revealed in 13F Filing — Google Stake Tripled.” May 2026. ibtimes.com

- BBAE. “13F Highlights: Where Top Investors Moved in Q1 2026.” 2026. bbae.com

- Berkshire Hathaway Inc. Form 13F-HR, Q1 2026. SEC EDGAR, filed May 15, 2026.

- StatCounter Global Stats. “Search Engine Market Share Worldwide.” Accessed May 2026. gs.statcounter.com

- StatCounter Global Stats. “Desktop Search Engine Market Share Worldwide.” Accessed May 2026. gs.statcounter.com

- ALM Corp. “Google Search Ad Clicks Just Hit a 5 Year High: Q4 2025 Benchmarks.” 2026. almcorp.com

- ALM Corp. “How Google’s SERP Remonetization is Reshaping Search: Data-Driven Analysis of Organic Decline and Paid Growth (2025-2026).” 2026. almcorp.com

- PPC Land. “AI still under 2% but growing: Datos Q1 2026 state of search report.” 2026. ppc.land

- Alphabet Inc. Form 10-K Annual Report, FY 2025. SEC EDGAR. sec.gov

- Alphabet Inc. Form 8-K Q4 2025 Earnings Release. SEC EDGAR. sec.gov

- Hunt, Jim. “Google’s AI Content Rules: What ‘Meet the Standards’ Actually Means.” Gridlok, May 2026. gridlok.co

- Hunt, Jim. “AEO Is Just SEO With New Acronyms (Here’s What Actually Changes).” Gridlok, May 2026. gridlok.co

See what ChatGPT is really searching

SubSeed captures the hidden Google queries ChatGPT runs behind every answer and enriches them with search volume, CPC, and keyword difficulty.

Related Posts

Make Gridlok a Preferred Source on Google

See Gridlok surfaced more often in your Top Stories, AI Overviews, and AI Mode. One click, applied across Google Search.